Variation C.2

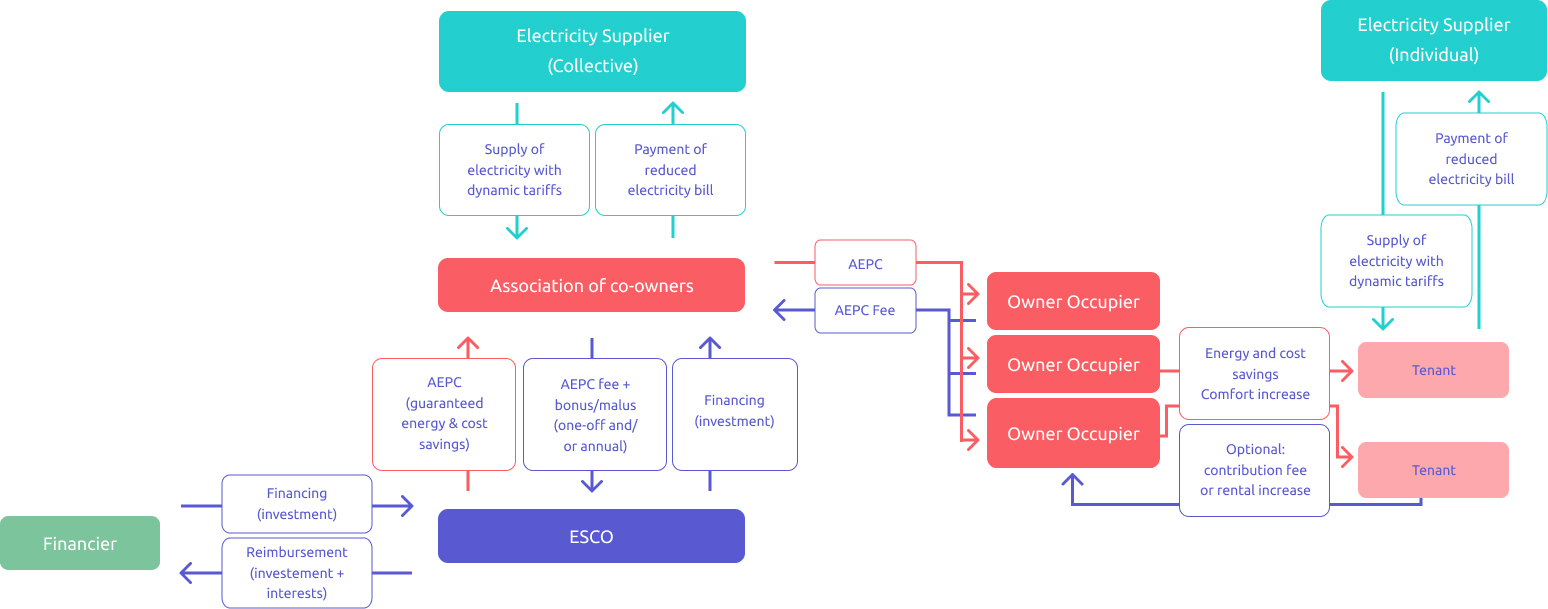

In this variation of the Business Model for collective apartment buildings, the main difference is situated in the apartment occupation. Some or a large number of apartments are not occupied by the building co-owners, but rather by other tenants who rent or lease the apartment from the co-owners.

The Active Building Energy Performance Contracting (AEPC) is still signed between the Energy Services Company (ESCO) and Association of Co–Owners (ACO), but in this Business Model variation, any energy savings from energy efficiency measures or building renovation, and cost savings from flexibility, will benefit the tenant or lessee, not the building owner. The co-owner will either have to pay for the investment from own funds or external financing (typically through the Financial Institution or ESCO) without any return on investment from the energy or cost savings. In this case, the decision to invest would mainly be driven by maintaining or improving the asset value of the apartment or the need to renovate the building that has maybe deteriorated beyond a point that rental prices become too low to represent a sound investment. In some cases, it may be the consequence of a large majority of co-owners having decided for the building renovation at the General Meeting of the Co-owners.

In some cases, the co-owner may negotiate a financial contribution by the tenant to the investment he is paying for. In this case he/she trades off an improvement in comfort against the return of part of the savings to his/her landlord who owns the apartment. This can be a one-off payment (e.g. a percentage of the investment cost paid by the owner) or an increase in monthly rent, agreed between both parties. If this is not possible, the apartment owner may need to wait until the end of the lease to increase the rent for the next tenant. The co-owner would take this into account when taking the decision of investing or when voting in favour of the project at the General Meeting.

Any cost savings coming from the flexibility are likely to benefit the tenant anyway as he/she is accepting the corresponding flexibility in comfort or usage and as the electricity contracts are with the tenant not with the co-owner.

From the Facilitator or the ESCO point of view, this presence of tenants – rather than only co-owners – represents an additional risk in the pre-contractual and contractual phase as some co-owners may decide not to go ahead with the project after all.

For the financier, there is not necessarily a large difference in comparison with the previous model, except the fact that some co-owners represent an increased credit risk, as they are not directly benefiting from the savings, but only from the increased building value. This may favour mortgage-based financing solutions.