Variation C.3

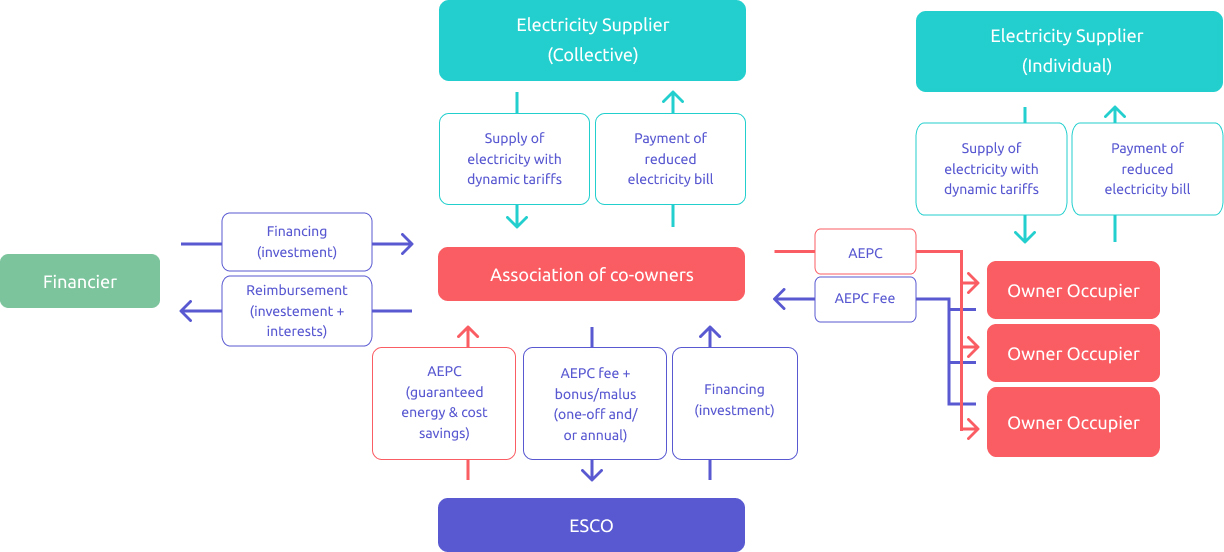

In this variation, the only difference is the fact that the financier directly finances the Association of Co–Owners (ACO), rather than the Energy Services Company (ESCO). As in the generic case, this shifts the credit risk from the ESCO to the Financial Institution (FI) which may be a more suitable solution, as a FI is probably better equipped to assess and manage risks at the level of an individual co-owner. Mortgage-based solutions are another familiar option for banks. They would already have a license for providing loans, which is much less likely to be the case for ESCOs unless the ESCO is specialized in this sector and obtains the necessary licenses to provide customer loans to residential apartment owners.

A mix of FI and ESCO financing is also possible as mentioned earlier for the generic model.

This FI financing variation could also apply to the case where there are a number of tenant lessees. In that case the increased credit risk of the owner lessor may again be more easily managed by a FI than by the ESCO. This case is he credit risk of the co-owner not being able to reimburse the loan directly shifts to the FI, away from the ESCO. This financing option may be preferred by the ESCO or can be implemented in case the ACO cannot obtain a collective loan. not depicted as it is just a combination of both previous models.